Global cross-border payments are at a pivotal juncture. In 2023, international transactions surpassed a staggering $190 trillion in volume, and forecasts suggest that by 2030, this figure could approach nearly $290 trillion. These numbers are not merely impressive—they highlight an urgent need to modernize the payments infrastructure that underpins global commerce. Traditional systems, many of which were built over 50 years ago, are increasingly burdened by slow settlement times, high fees, and fragmented processes. At the same time, rising costs for accessing dollars, shifts in global trade corridors due to political tensions, and the emergence of new markets are pushing the boundaries of what legacy systems can handle.

At Altara, we see the evolution of cross-border payments not only as a necessary adaptation to a changing economic landscape but also as an unprecedented opportunity for innovation.

In this article, we explore how the payments stack has evolved—from legacy banking and traditional card networks to real-time payments and closed/semi-closed loop wallets, and now to blockchain-based stablecoins. We examine how stablecoins work (including their mechanisms for maintaining stability), why they are gaining traction now, how regulators are reacting, and where we see significant opportunities for future investment.

The evolution of global payments is a story of continuous innovation, with each phase addressing the limitations of its predecessor while paving the way for new technologies.

In the 1970s, the introduction of systems like ACH and SWIFT revolutionized international finance by enabling banks to transmit payment instructions across borders. These early networks enabled the expansion of global trade by providing a standardized method for transferring funds internationally. However, they were designed for an analog era with significantly lower transaction volumes. Today, legacy systems reveal several critical limitations:

Fragmentation: No unified global standard exists, resulting in a patchwork of regional protocols.

Multiple Intermediaries: Payments often pass through several banks, clearing houses, and FX brokers. A typical international wire might involve three or more intermediaries, each adding delays and fees.

Slow Processing: Settlement times generally range from 2 to 5 days. According to a McKinsey report, processing delays in traditional cross-border payment systems have significantly increased over the past two decades.

High Costs: International wire fees range between $30 and $50 per transaction, with remittance fees averaging around 6.35%, and sometimes even reaching 8% in specific corridors.

Following the era of legacy banking, global payment networks such as Visa, Mastercard, and digital platforms like PayPal emerged. These systems transformed consumer payments by offering enhanced security and rapid transaction processing domestically. For instance, Visa now processes over 500 million transactions per day. Additionally, closed/semi-closed loop wallets such as Alipay, PayPal, and rail aggregators such as Wise have built robust ecosystems that enable consumers to manage their funds seamlessly. Although these networks have dramatically improved domestic payments, they still rely on legacy infrastructure for cross-border transactions, leading to similar inefficiencies in international settlements.

The advent of real-time payment (RTP) systems has further advanced the payments landscape. Domestic RTP systems, such as India’s Unified Payments Interface (UPI), the US's FedNow, and Brazil’s PIX, enable transactions to settle in seconds, drastically reducing delays and costs. Fintech disruptors like Wise, Nium, and Thunes have built on these systems, improving the user experience by pooling liquidity and offering near-instant international transfers. However, scaling RTP systems across borders remains challenging due to:

Interoperability Issues: RTP systems are often designed for domestic use and require complex integrations to function internationally.

Fragmented Infrastructure: Varying regulatory frameworks and technical standards across countries complicate cross-border interoperability.

Limited Scalability: Coordinating multiple RTP networks to achieve seamless global coverage increases costs and can reintroduce delays.

As global payments have grown more complex, the need for a unified messaging standard has become apparent. ISO 20022 has been created as the global standard for financial messaging, replacing older formats like SWIFT MT. This standard facilitates more efficient, transparent, and automated processing of payments. Its adoption is critical for modernizing legacy systems and enabling better interoperability between traditional banks and new digital payment platforms. ISO 20022 is now being implemented by major global financial institutions and central banks, ensuring that the messaging used in cross-border payments is both consistent and future-proof.

SWIFT's deadline for major banks to transition to ISO 20022 is November 2025, with it planning to phase out MT (the current standard), from that month on. The industry expects SWIFT to develop contingency plans that would allow a smaller subset of participants to continue using MT for a short period of time or utilise conversion tools to prevent disruptions to the global rollout of ISO standards.

Over the past decade, billions of dollars have been invested in blockchain infrastructure, giving rise to stablecoins. Initially used by crypto traders to hedge against volatility, stablecoins like USDC and USDT have evolved into a scalable, cost-effective settlement layer.

Unlike RTP systems that are confined by regional infrastructure, stablecoins operate on a unified public blockchain. This global unified network can leverage universal payment standards such as ISO 20022—a messaging protocol compatible with all settlement mechanisms. As ISO 20022 becomes more widely adopted, traditional financial services can more easily integrate with and adopt stablecoin-based infrastructure, allowing them to quickly shift payments from multi-intermediary systems to direct, stablecoin-based transfers.

This evolution marks the latest phase in cross-border payments, offering a solution that is faster, cheaper, and more reliable than conventional systems.

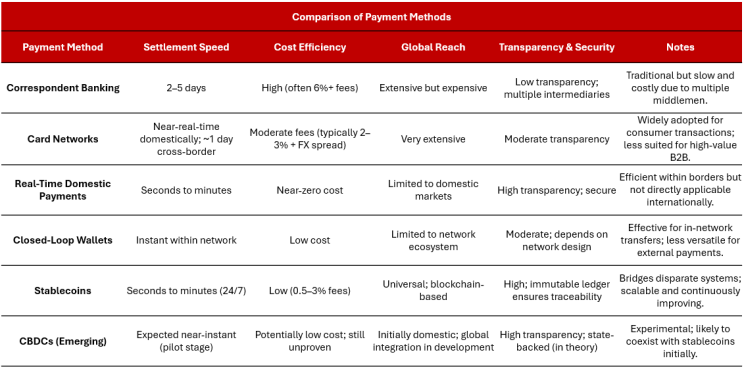

Stablecoins are emerging as the new backbone of modern cross-border payments. They offer the stability of traditional fiat currencies while leveraging the speed and cost-efficiency of blockchain technology.

Stablecoins are digital tokens pegged to a reference asset—typically a fiat currency such as the US dollar—designed to maintain a stable value. This peg makes them an attractive medium for everyday transactions, as they provide the predictability required for business and consumer use. Unlike volatile cryptocurrencies, stablecoins offer a consistent value, making them ideal for cross-border settlements and large-scale financial transactions.

Stablecoins employ several methods to maintain their value:

Fiat-Collateralized Stablecoins: These tokens, such as USDC and EURC, are backed 1:1 by fiat reserves held in regulated bank accounts. Regular third-party audits ensure that reserves are maintained at or above 100%, instilling confidence in the peg.

For example, Circle ensures that USDC and EURC reserves are maintained separately from its operating funds, and detailed reserve reports have been published since 2018, with SEC filings in 2021 and 2022. Additionally, USDC reserve holdings and mint/burn flows are disclosed weekly, and a Big Four accounting firm provides monthly third-party assurance (per AICPA standards) that the reserve value exceeds the circulating supply, thereby instilling strong confidence in the 1:1 peg.

Crypto-Collateralized Stablecoins: Tokens like DAI use cryptocurrencies as collateral and are typically over-collateralized by 150% or more to buffer against volatility. Smart contracts dynamically manage collateralized debt positions (CDPs) to adjust for fluctuations in the underlying asset’s value.

Algorithmic Stablecoins: These stablecoins rely on algorithmic mechanisms to automatically adjust the supply based on market demand. When the token price deviates from its target, the algorithm increases or decreases the supply to restore the peg. Although innovative, algorithmic stablecoins have faced challenges in maintaining stability during periods of market stress.

Stablecoins are experiencing explosive growth. According to Visa Onchain Analytics:

Transactions: Over the past 12 months, total transaction volume reached $33.2T (Visa's total volume for 2024 was $13.2T), with an adjusted transaction volume of $6.1T in the past 12 months across 5.1 billion and 1.3 billion transactions respectively. Volume is up 58% and transactions 35% over the last 12 months.

Market Supply: As of March 2025, the aggregate supply is approximately $212.6 billion.

These figures illustrate the rapid mainstream adoption of stablecoins, driven by their advantages:

Speed: Settlement occurs in seconds, enabling rapid cross-border transfers.

Cost Efficiency: Fees typically range from 0.5% to 3.0%.

Global Reach: Operating on public blockchains, stablecoins transcend regional limitations.

Transparency & Security: An immutable public ledger ensures full traceability and minimizes fraud.

Several factors are converging to accelerate the adoption of stablecoins:

Expensive Access to Dollars: Global markets are experiencing rising costs for accessing US dollars due to tighter monetary policies, increased demand, and supply constraints. This makes traditional channels less attractive, positioning stablecoins as a cost-effective alternative.

Emerging Trade Corridors: Political tensions and shifting geopolitical alliances are creating new trade corridors. In these emerging corridors, traditional payment systems often struggle due to outdated processes and fragmented regulatory environments. Stablecoins, with their unified global protocol, offer a seamless and scalable solution.

Demand for Speed and Efficiency: As global trade accelerates, there is an increasing need for fast, reliable, and low-cost transactions. Stablecoins settle in seconds, drastically reducing the time and expense associated with cross-border payments.

Economic and Political Uncertainty: In an era of economic volatility and political instability, stablecoins provide a secure, predictable means of transferring value globally, which is particularly appealing for businesses and consumers looking to mitigate risk.

As stablecoins become an integral part of the global payments ecosystem, regulators worldwide are adjusting their frameworks to manage these new technologies. A robust regulatory environment is essential for building institutional confidence and ensuring the secure operation of digital payment systems.

In February 2025, the United States Senate Banking Committee introduced the GENIUS Act to the floor as proposed legislation, which sets a comprehensive regulatory framework for stablecoin issuers. Key provisions include:

These measures are designed to protect the integrity of the US dollar while encouraging innovation in the digital payments space. Early industry feedback suggests that compliance with the GENIUS Act has led to an increase in institutional interest in stablecoin projects.

The European Union’s Markets in Crypto-Assets (MiCA) regulation, which became effective in December 2024, offers a harmonized regulatory framework for stablecoins across member states. MiCA aims to:

MiCA's unified regulatory environment is seen as a way to reduce compliance costs for cross-border transactions, facilitating smoother integration of stablecoin-based systems across Europe.

Other key regions have also updated their regulatory frameworks:

These regulatory initiatives are vital for mitigating systemic risks and building the institutional trust necessary for widespread adoption of blockchain-based payment systems.

Understanding the modern payments stack is critical to appreciating how stablecoins are transforming global finance. The payments stack comprises several key layers, each playing a distinct role in the overall ecosystem.

The settlement layer is the backbone of the payments system, consisting of the blockchain infrastructure that processes transactions.

Key Players:

Function: Provides a decentralized network that processes and settles transactions rapidly. For example, upgrades such as Ethereum’s Dencun have reduced transaction costs by up to 90% in some scenarios.

Asset issuers are responsible for creating, managing, and redeeming stablecoins.

On/off-ramp providers bridge the gap between fiat currencies and stablecoins.

Digital wallets like Alipay, PayPal, and Wise play an essential role in facilitating payments.

The final layer comprises user-facing applications.

Stablecoin settlement leverages blockchain technology to streamline the process:

This efficient process starkly contrasts with traditional cross-border transfers that require multiple intermediaries and manual reconciliation.

The global cross-border payments market represents a multi-trillion-dollar opportunity, and stablecoins are uniquely positioned to capture a significant share. Based on extensive research and data analysis, Altara identifies several key investment areas.

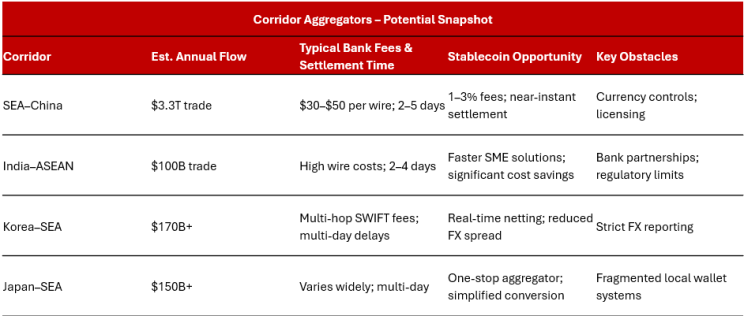

Many international trade corridors continue to suffer from outdated processes and fragmented regulatory frameworks. Aggregator platforms that focus on specific corridors can bridge these inefficiencies by securing local licenses, partnering with regional banks and digital wallet providers, and deploying APIs that seamlessly integrate domestic payment systems with stablecoin-based settlement layers.

Key Data Points:

SEA–China Corridor: Intra-Asia trade in this corridor reached approximately $3.3 trillion in 2023, with SMEs often burdened by high fees and prolonged settlement times.

India–ASEAN Corridor: Trade volumes exceed $100 billion annually, with legacy banks charging $30–$50 per transaction and settlement times ranging from 2 to 4 days.

Korea–SEA Corridor: Bilateral flows exceed $170 billion, yet multi-hop processes in traditional systems significantly delay settlements.

By targeting these corridors, aggregator platforms can dramatically reduce settlement times—from days to minutes—and lower transaction fees, providing a compelling advantage to both SMEs and larger trading enterprises.

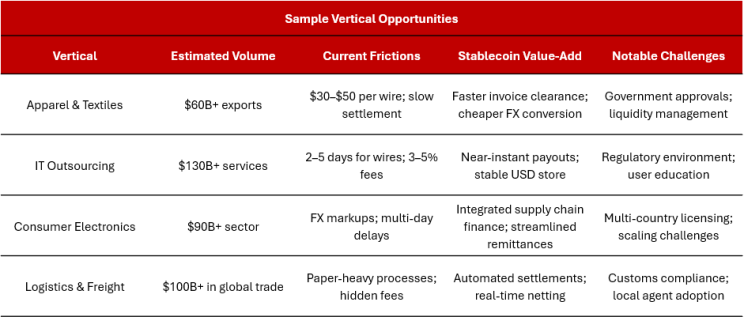

Vertical platforms that integrate stablecoin settlements into specific industry workflows offer significant investment opportunities. By focusing on particular sectors such as apparel, IT outsourcing, consumer electronics, or logistics, these platforms can address unique friction points—such as high transaction fees, FX volatility, and lengthy settlement times—while integrating additional value-added services.

Key Data Points:

B2B Transactions: B2B payments account for nearly 80% of global cross-border payment revenue, totaling over $150 trillion annually.

Industry-Specific Challenges: In apparel-exporting regions like Bangladesh and Vietnam, SMEs can incur wire fees ranging from $20 to $100 per transaction, which significantly impacts cash flow.

IT Outsourcing: In markets between India and the Philippines, stablecoin payouts can save $5–$10 per $200 transfer.

Vertical solutions not only improve operational efficiency but also build durable competitive moats by integrating services that are difficult to replicate with generic platforms.

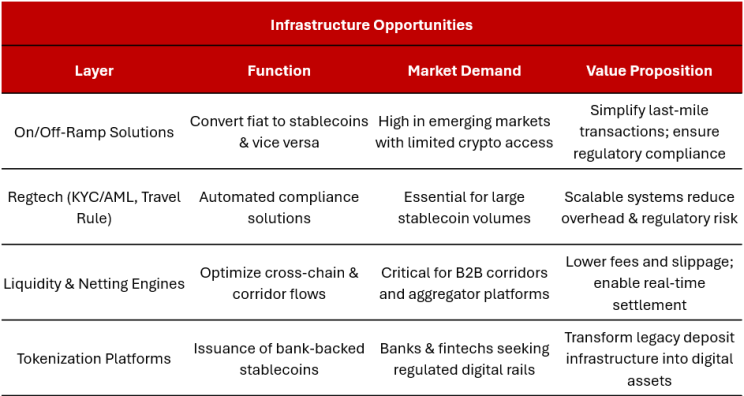

A mature stablecoin ecosystem relies on robust foundational infrastructure. The “picks & shovels” segment includes:

On/Off-Ramp Solutions: Technologies that enable seamless conversion between fiat and stablecoins are critical, especially in regions with limited banking infrastructure.

Regtech Solutions: Automated compliance systems for KYC/AML and Travel Rule enforcement can reduce regulatory overhead, which in traditional systems may account for 5–10% of revenues.

Liquidity & Netting Engines: Platforms that optimize cross-chain liquidity and facilitate efficient netting of transactions can significantly reduce slippage and fees, particularly in high-volume B2B corridors.

Tokenization Platforms: Systems that allow banks to issue digital tokens representing fiat deposits—“tokenized deposits”—provide a crucial link between legacy financial systems and modern blockchain networks.

Investing in these foundational technologies is essential for scaling the stablecoin ecosystem and ensuring its long-term viability.

Traditional banks are increasingly exploring digital innovations by issuing “tokenized deposits”—stablecoins that represent fiat currency held in bank reserves. This approach merges the trust and regulatory oversight of conventional finance with the efficiency of blockchain technology. Pilot programs in Japan, Korea, and Singapore have shown that banks can issue digital tokens that facilitate faster cross-border transfers. For technology vendors, creating platforms that bridge legacy banking systems with blockchain-based tokenization solutions represents a significant growth opportunity. As banks continue to modernize their payment systems, the demand for secure and compliant stablecoin solutions will only expand.

Stablecoins are emerging as a universal settlement layer that bridges advanced domestic payment networks with the nascent world of central bank digital currencies (CBDCs). Domestic systems such as Brazil’s PIX, India’s UPI, and Europe’s SEPA Instant enable fast and low-cost transactions within national borders, but extending these efficiencies internationally has proven challenging due to differing legal and technical frameworks.

Stablecoins offer a solution by converting local fiat into a digital asset that can be transmitted globally over a unified blockchain and then re-converted into local currency at the destination. This process bypasses the need for direct bilateral integrations between every national system and is particularly valuable in regions where regulatory or technical fragmentation impedes cross-border connectivity.

At the same time, CBDCs—like China’s e-CNY and projects such as the multi-CBDC mBridge connecting Hong Kong, Thailand, the UAE, and mainland China—are gaining traction. Although CBDCs promise enhanced security and regulatory oversight, they are still in their experimental stages and may initially coexist with stablecoins. Many experts expect that stablecoins will handle everyday retail and B2B transactions, while CBDCs facilitate larger interbank transfers, until a fully integrated global system emerges.

The evolution of global cross-border payments represents a profound transformation in the way value is transferred worldwide. With transaction volumes projected to approach $290 trillion by 2030, the potential for disruptive change is immense. Traditional systems, characterized by slow settlements, high fees, and fragmented processes, are rapidly being outpaced by blockchain-based solutions that offer near-instantaneous settlements, drastically lower costs, and superior scalability.

Stablecoins lie at the heart of this transformation. Their ability to settle transactions in seconds—with fees between 0.5% and 3.0%, compared to up to 6.35% for conventional methods—provides a compelling economic advantage. Furthermore, the unified, global nature of blockchain networks enables stablecoins to scale effortlessly across international corridors. This is a stark contrast to traditional RTP systems, which are hindered by interoperability issues and regional fragmentation.

The current surge in stablecoin adoption is driven not only by their inherent technological and economic benefits but also by broader macroeconomic factors. Rising costs of dollar access, the emergence of new trade corridors driven by political tensions, and the pressing need for speed and efficiency are accelerating the shift toward stablecoin-based settlements.

Regulatory advancements, including the proposed GENIUS Act in the United States and MiCA in the European Union, are establishing a supportive framework that reduces systemic risk and bolsters institutional confidence. These frameworks, coupled with significant technological improvements, are laying the groundwork for a new, efficient, and transparent global payments ecosystem.

At Altara, we are excited by these trends. The evolution of cross-border payments has opened up numerous micro-level opportunities—from corridor infrastructure providers and industry-specific verticals to essential “picks & shovels” and hybrid models that merge traditional finance with blockchain innovation. The data is compelling: stablecoins and blockchain-based payments are not merely alternatives to legacy systems—they represent the foundation of a new global payments network that promises to be faster, cheaper, and more transparent.

For investors and innovators ready to embrace this transformation, the opportunity to reshape global cross-border payments is both compelling and imminent. At Altara, we remain committed to identifying and supporting the disruptive technologies that will drive the next wave of financial transformation.

An Altara Perspective

This article has traced the evolution of cross-border payments—from the early days of legacy banking and SWIFT (including advancements like SWIFT gpi) to modern closed and semi-closed loop wallets (such as Alipay, PayPal, and Wise) and the revolutionary potential of blockchain-based stablecoins. We have integrated historical context, detailed technological analysis, robust economic data, and insights into regulatory developments to outline a data-driven path forward for global finance. Stablecoins, with their unmatched speed, cost efficiency, and scalability, are poised to become the foundation of a new global payments network. For investors and innovators ready to lead this transformation, the opportunity to reshape global cross-border payments is both compelling and imminent.